Silver, down but not out.

Silver has undergone a massive adjustment in speculative positioning with the physical supply shortage met by falling COMEX bullion vault holdings, supporting my tactical sell silver calls strategy.

Since its peak at USD 121.64/oz on the 29th of January, the price of silver has corrected by 50%, falling to a low of USD 60.94/oz before stabilizing. While momentum indicators continue to suggest scope for weakness, so far, it’s held above its 200-day moving average (USD 50.50/oz), with the decline in the price of silver appearing to be largely driven by an unwind of speculative positions, with fundamental drivers and supply-demand dynamics more supportive.

The correction in silver appears to have been driven by a confluence of events. Starting in the Autumn, we saw a decline in holdings of bullion in COMEX approved vaults. Pressure on silver intensified from the Festive Season through to early February, when the Chicago Mercantile Exchange (CME) moved to an ad valorem margin requirement, pushing my estimate of the margin requirement up from 6.1% of the notional value of the contract pre-Christmas, up to a peak of 18%. And from the end of February, we’ve seen a further unwind of positions owing to the Iran-Israel/US war. These events triggered a substantial correction in positions as evidenced by a decline in trading volume and non-commercial net open positions in the 5,000oz contract trading on the CME, a decline in bullion held in COMEX approved vaults, a move in the forward price of silver into contango – consistent with a decline in silver leasing rates to near-zero – and price weakness.

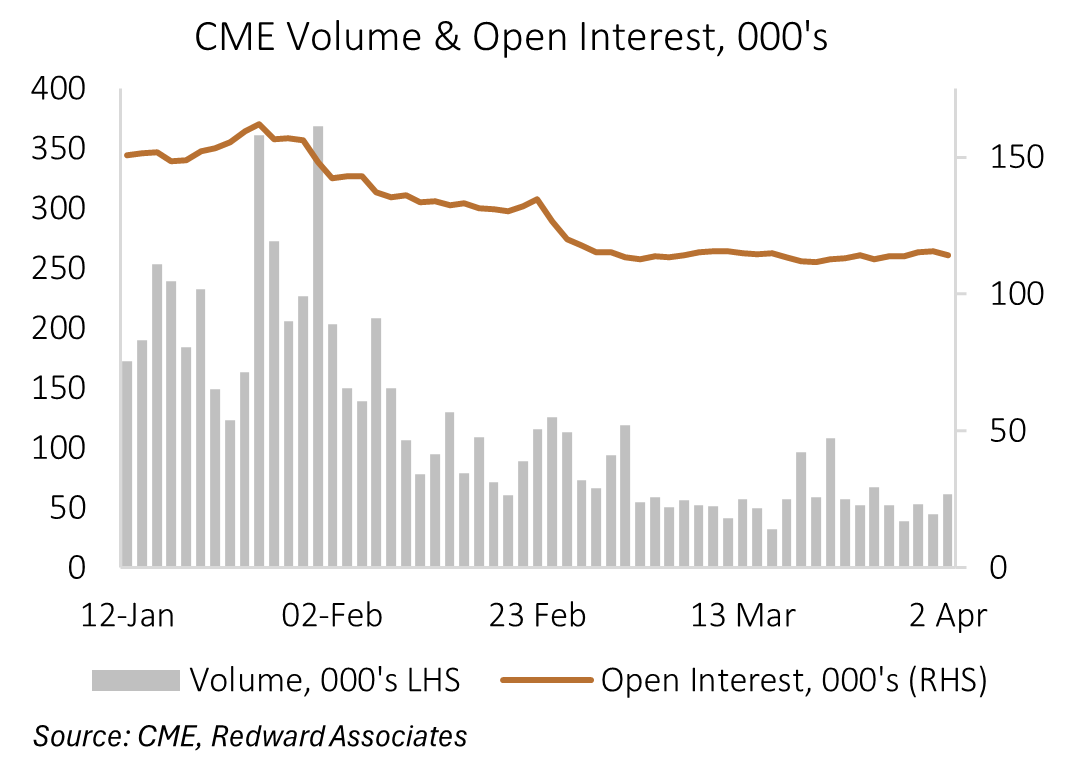

Weakness in futures…

Average daily trading volume in the 5,000oz silver futures contract is down 72% between the second half of January and the second half of March. This is despite the price of silver falling 27% and the CME lowering the silver margin requirement 4pp, to 14%, with the combined effect lowering the US dollar value of margin required by 44%.

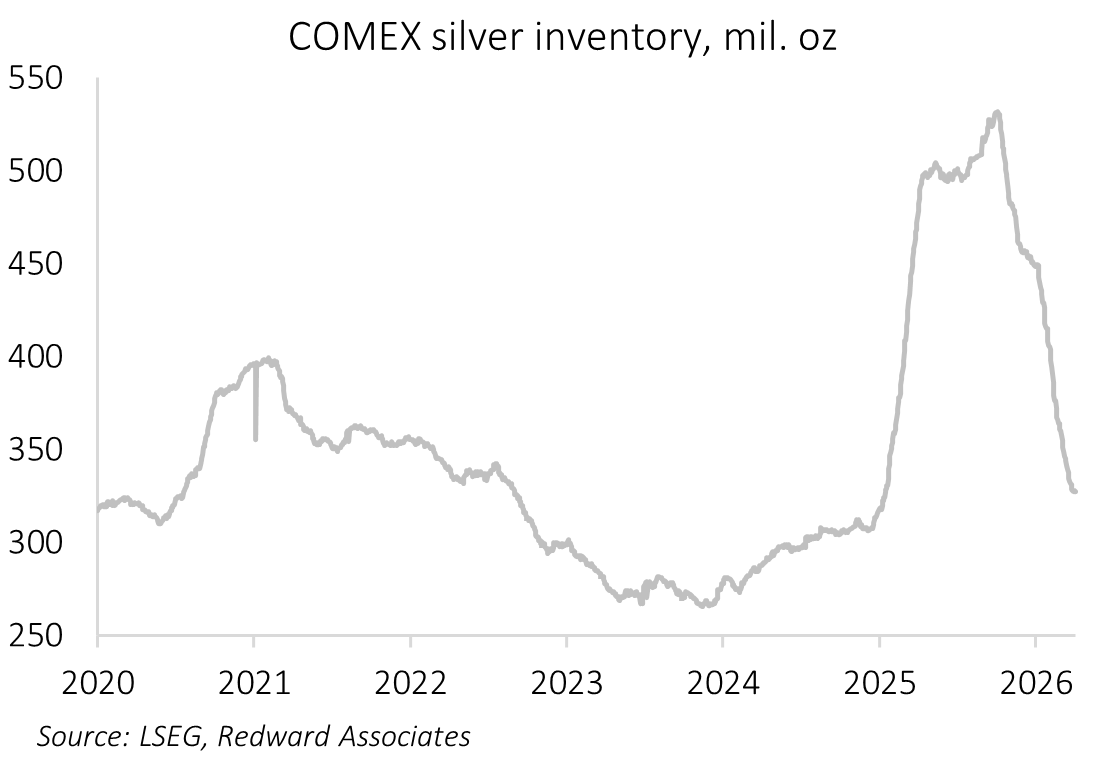

Net open non-commercial positions in silver stabilized in March at 116Moz, down 27Moz from year-end. The decline in US investor interest in silver is also evident in bullion held in COMEX approved vaults. Vault holdings peaked on the 3rd of October 2025, at 531.9Moz, and has subsequently declined 204.2Moz.

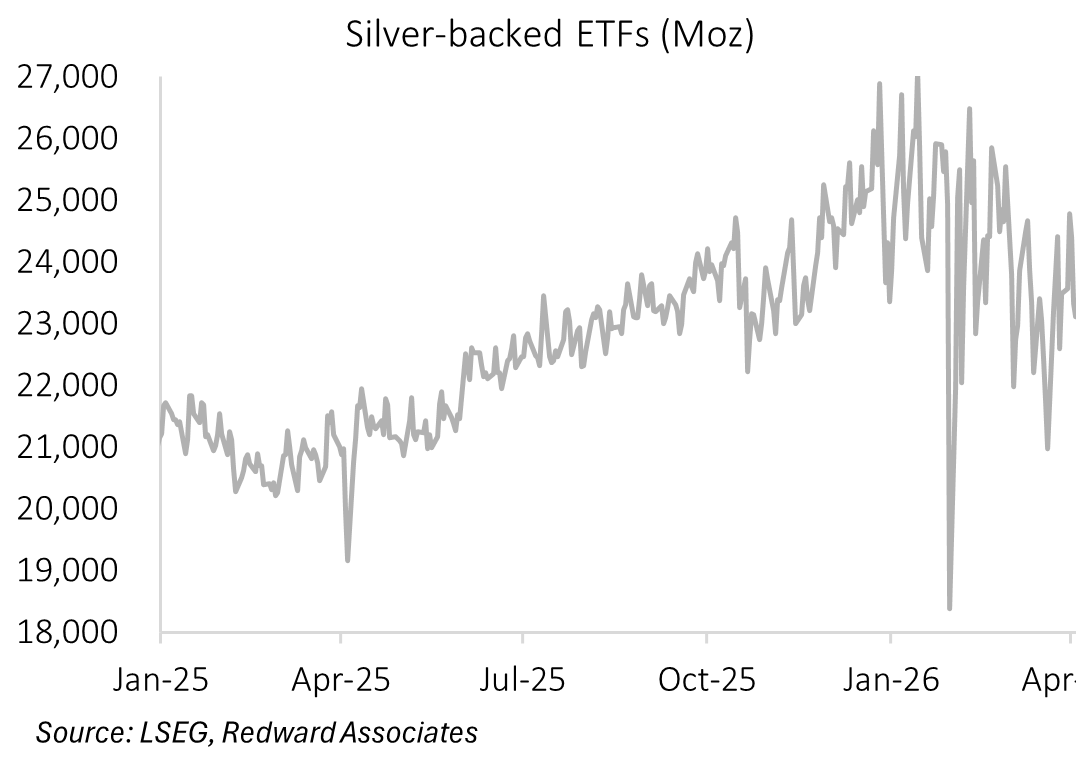

…Stability in ETFs…

My estimate of silver-backed ETF holdings is based on daily reporting from four key ETFs (iShares Silver Trust, ABRDN Physical Silver ETF, Wisdomtree Silver ETC, Sprott Physical Silver Trust). My estimate has been quite volatile in recent months, with aggregate holdings falling around 128Moz from their year-to-date peak to around 745Moz, but holdings appear to be stabilizing.

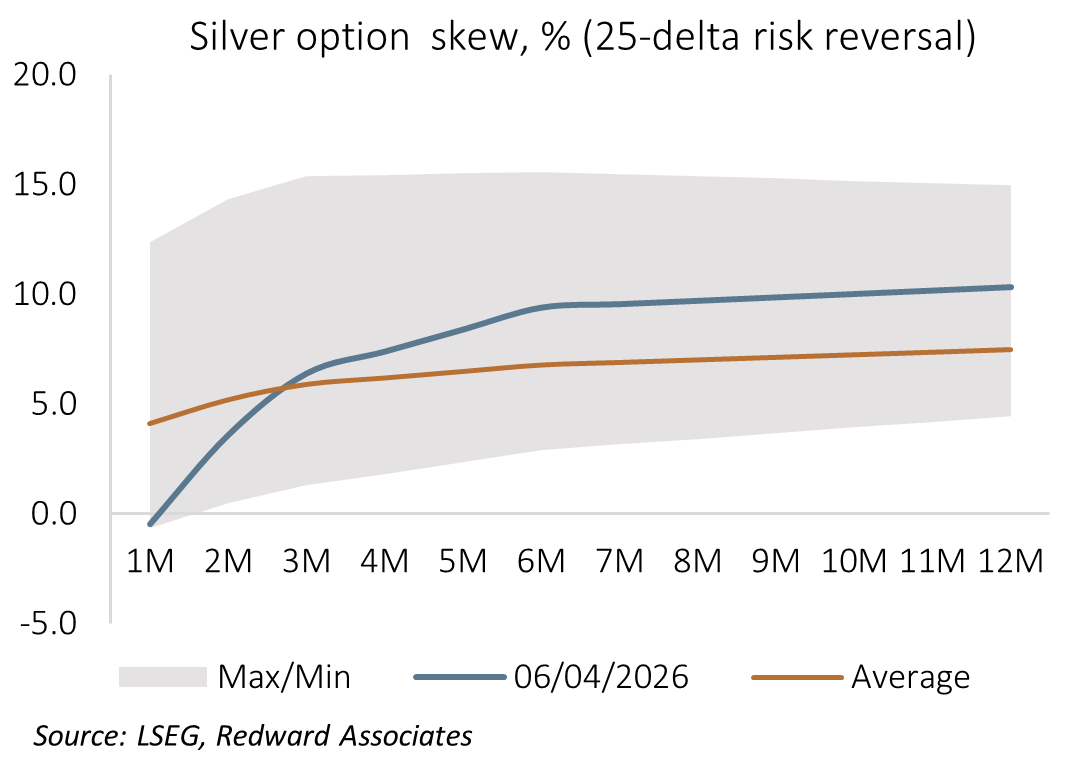

…Push-pull in options…

The decline in the price of silver has occurred in conjunction with a decline in silver implied volatility, with one-month at-the-money forward implied volatility falling to around 65% from above 90% through late January/early February. While the decline in implied volatility is material, it remains well above its past decade average (26%), suggesting the silver market remains highly unstable.

This instability is evident in option volatility skew. After hovering as high as 12% in favor of US dollar call options through end-February/early March, the one-month 25-delta risk reversal skew has tumbled to -0.8%, suggesting scope for near-term weakness. However, while the options market sees scope for near-term weakness, option skew is strongly in favor of silver call options beyond one-month, with twelve-month 25-delta option volatility skewed 10.3% in favor of silver calls, well above its past decade average of 2.8% (average is past 12-months).

…risk aversion…

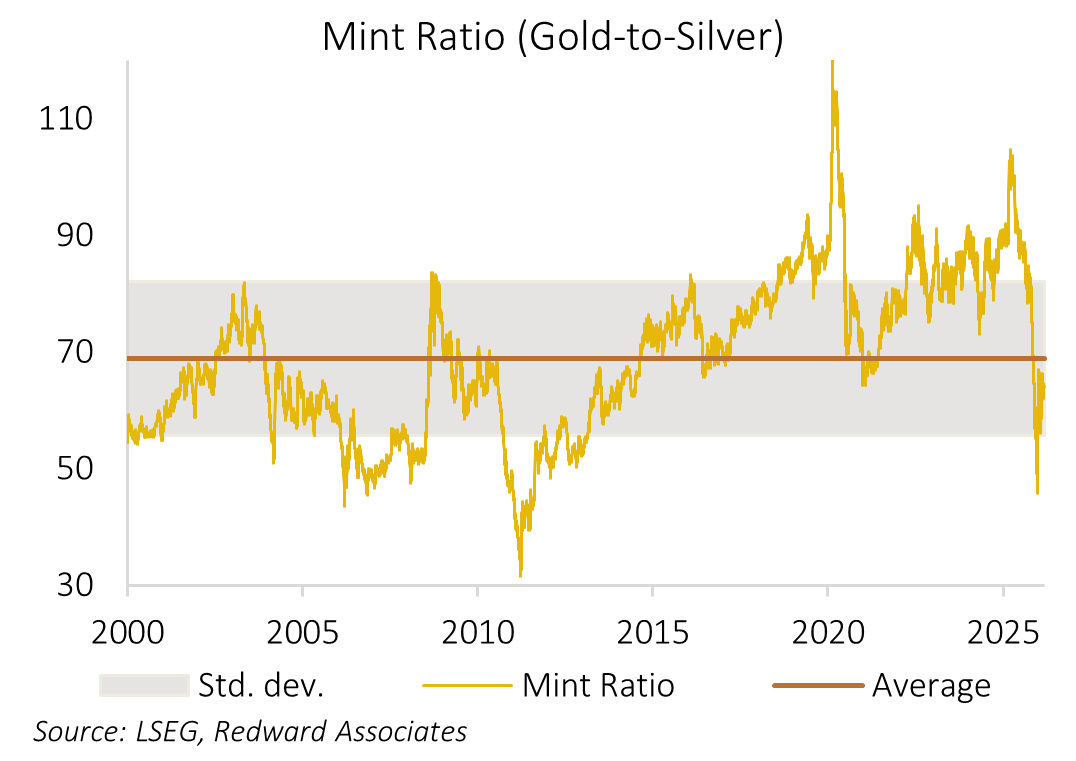

As silver is both a precious and industrial metal and its market liquidity is considerably lower than gold, the Mint Ratio – the ratio of gold-to-silver tends to be sensitive to both demand for precious metals and global economic growth expectations. This pattern of behavior has been evident recently, with the Mint Ratio rising from a cyclical low of 46:1 in late January to around 64:1 currently.

…but longer-term support

However, it isn’t clear that consumer and industrial demand for silver will necessarily decline. Traditional uses of silver in photography and silverware have declined substantially over the post-millennium period, while use of silver in green energy is becoming increasingly important. The fact that silver has the lowest electrical resistance of all metals makes it ideal for use in photovoltaic cells, with demand projected to be around 195Moz this year, absorbing around 24% of mine production. Silver is also heavily used in other electrification devices, notably electric vehicles.

So, while the crisis in the Middle East might point to weaker demand for jewelry and traditional industrial uses, this may be offset by renewed demand for solar panels and electric and hybrid vehicles.

Below, I discuss my investment thesis and trade ideas.

The following content is for paid subscribers only.

I’m not brash in how I market my work. I enjoy writing these articles and I would like to think the work speaks for itself. If you enjoy my work, please consider a paid subscription, where you will receive my thoughts on trading ideas in precious metals.

If you would like to read this article, you can, for just US$ 15 for a one-month subscription, or US$ 150 p.a. That works out at about a dollar an article